2026-03-26

February 2026 continued the strengthening trend that began late in Q4 and accelerated through January, reinforcing the seasonal lift that typically emerges as the industry moves into spring.

Dealer sentiment across the country remains optimistic, with most retailers describing the market as much better than it was at the same time last year. Dealer new unit inventory levels have improved significantly compared with February 2025, easing some of the pressure created by elevated stock levels over the past two years.

While margins on new units remain tight, new unit retail sales are noticeably stronger than in the first quarter of 2025. The broader economic backdrop still carries a degree of uncertainty, driven by rising prices at the pump and the growing tensions in the Middle East, but those concerns did not materially impact powersports demand in February.

Wholesale Pricing Strengthens

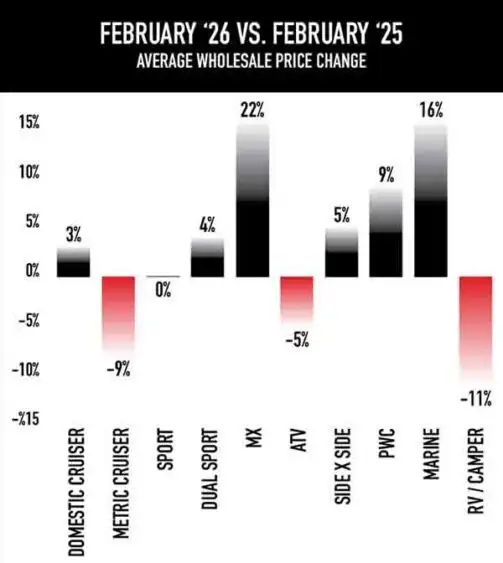

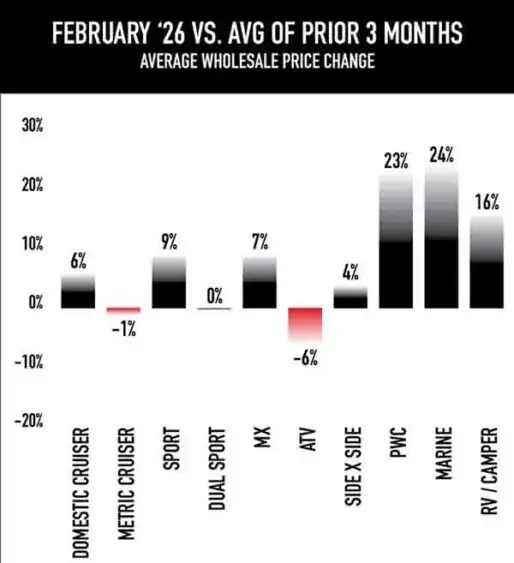

Wholesale pricing trends in February 2026 reflected this improving retail narrative, with most key categories strengthening both year-over-year (YoY) and compared to the trailing 90-day average.

Domestic Cruisers led the charge, with Actual Wholesale Price (AWP) increasing 3% YoY and 6% versus the prior 90 days, highlighting strong dealer demand for used H-D product. Sport bike pricing also displayed a significant seasonal uptick, up 9% from the last three months.

Off-road categories followed suit in MX and Side-by-Sides, outperforming 2025. Larger dollar specialty units also saw a significant rise over the trailing 90-day average. Marine and RV pricing, fueled by increased bidder activity and buyer demand, improved significantly coming out of the winter months.

Overall, February’s pricing metrics confirm that wholesale values are firming sequentially as dealers prepare inventory for the spring riding season.

Spring Market Outlook

Looking ahead to the next 30–60 days, historical trends suggest wholesale values should continue to strengthen as retail demand accelerates into March and April. The improving balance in dealer inventory – particularly the significant YoY declines in new Side-By-Side inventory – is helping remove some of the downward pressure that affected used pricing throughout much of 2024 and 2025.

For dealers, prioritizing acquisition of clean pre-owned units, maintaining tight control over aging inventory, and positioning inventory mix ahead of the peak riding season will remain critical. If current trends continue, February 2026 may represent the point where the market transitions from stabilization into expansion, setting the stage for a very solid spring selling environment.